#14.Before You Go Manufacture

And many other lessons.

This is a subscribers only article for my newsletter.

Just finished the last exam for the term. I am currently reading a lot about Japanese Lean Manufacturing for a paper due next week. It got me thinking about all my manufacturing experiences and lessons learnt.

My first experience was at Ford Motor Company in Essex, UK. This was very insightful, and I hope to explore it in a separate article soon. The second experience was at a consumer goods manufacturing startup in Lagos, Nigeria. I came onboard the project when the equipment had just arrived.

Over the next 2month period I got the opportunity to support the installation of the machines, get involved, and kick-off production. I also participated in the sales and marketing visit to retailers and major markets across Lagos, Nigeria.

It was a profound experience.

Eventually I began to flirt with the idea of starting my own manufacturing company. Something focused on processing agricultural raw materials into finished products. Halfway into preparing a business plan I made an interesting discovery.

I discovered a number, an equation, anyone can use to succeed in any manufacturing project, called

The Breakeven Point (BEP).

Let’s dig in.

The Breakeven Point (BEP).

Every manager or businessperson has asked at least once “At what point do we break even?”

A quick way to answer this is the breakeven point analysis.

The breakeven point (BEP) or breakeven quantity tells you the number of additional units(quantity) you need to sell to recover your cost or ‘break-even’. The quickest way to understand this is to work through how the equation is derived and practice an example.

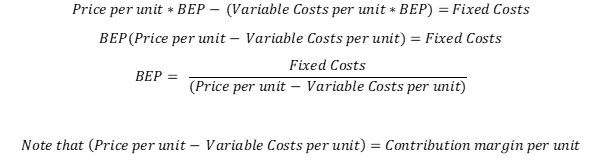

(1) - At the point of break even, profit equals zero, and Total Revenue = Total Cost

(2) - We then introduce the BEP – which is a unit quantity to both sides of the equation as the number of units sold affects both the revenue the firm makes and the cost it incurs to earn it. Revenue is the unit quantity sold multiplied by the unit price.

(3) – You reorder the equation and solve for BEP

Hence, BEP can also be written as

To calculate BEP you need to know the fixed costs and the contribution margin per unit (variable costs and selling price).

Note: variable costs are per unit costs that vary with a company’s production volume. They rise when you increase production and fall as production decreases.

Fixed Cost are those that irrespective of a change in production you must pay for such as rent, advertising, new equipment, and office supplies.

Let’s apply this to 2 examples.

Example 1

A company sells each pair of its shoes for $34.00. The variable cost to make each pair of its shoes is $24.00. The fixed cost to produce the shoes is $2,000. Let’s say this fixed cost is a new shoe machinery. So how many shoes does the company need to sell to breakeven on its production expense?

Let’s use the equation:

So, if the manager of this company believes he can sell over 200 extra pairs of shoes because of this new shoe machinery, recoup their costs, then this is a worthwhile investment. But if he doesn’t believe that an investment in this new machine will yield enough incremental demand for their shoes, then it isn’t a good investment. It will not breakeven.

Example 2

NeroCompany Ltd manufactures a product with a selling price of $28 per unit. Its variable cost per unit is currently $12 and its monthly fixed production overheads are $48,400. It currently sells 8,000 units per month.

a. What is the company’s monthly break-even point (BEP)?

b. What is the company’s profit per month?

How do companies use BEP?

Managers can use BEP to evaluate different What if scenarios.

- What if we change the price? How many more (or less) quantities would we sell?

- What if we want to make an investment and increase the fixed costs e.g increase capacity or get a bigger facility?

- What if we change the variable cost of producing our product?

BEP can be used to evaluate any investment decision.

Unlike other common approaches like calculating internal rate of return (IRR), investment payback period, and net present value analysis, breakeven analysis is easy to understand and apply.

Price Change

So, for the example of evaluating a potential price change, BEP is useful in determining the required additional demand to justify the price change:

For example, let’s assume your current demand is 100 units at a current price of $12.00, but you want to decrease your price by $2.00.

If your product has a contribution margin of $5.00(at the $12.00 price), therefore, contribution margin at new price of $10.00 is $3.00($5.00 - $2.00)

So, to justify the lower price, you have to be sure you can sell an additional 67 units.

Marketing

I know I talked about manufacturing, but the biggest application of breakeven analysis currently, is in marketing.

It can be used to decide on a new marketing campaign, and pricing (like above). So, for a new campaign, how much additional demand and hence sales do you expect?

Doing a social media marketing campaign? Same. How much return do you expect from sponsoring that post? All you have to do is swap fixed cost for the marketing cost and your expected margin for contribution margin.

Conclusion

In this article we have learnt about fixed cost, variable cost, contribution margin, and Breakeven Point (BEP) analysis. Understanding how costs behave is crucial for effective planning.

This article is called Before you go Manufacture but then again you could have swapped Manufacture for anything: Before you go Marketing, Before you go Selling. This universal tool can be applied to anything, especially marketing.

So, next time you need to make an investment, pricing, or marketing decision, consider using Breakeven Point (BEP) analysis,

Before you go…

I hope you found this informative and relevant, and I look forward to hearing about how you apply this.

You can catch up with past articles in this newsletter HERE

You can also email me at notesbynero@gmail.com or follow me on LinkedIn, and Instagram.

I recently published a Table of Content to all my writing, which I would update regularly.

Stay Tuned.